Corporate Tax in UAE: A Complete (In-Depth) Guide

Understanding corporate tax in UAE is essential for businesses operating within the country, whether you’re a startup, an SME, or a multinational corporation. With the recent changes to the United Arab Emirate’s tax landscape, including the introduction of a corporate tax rate and various tax exemptions, it is crucial to stay informed about the latest regulations and filing requirements.

The UAE’s tax policies are designed to foster economic growth, encourage foreign investment, and ensure compliance with global tax standards, making it vital for businesses to adapt to these new frameworks. This article provides a comprehensive overview of the key aspects of corporate tax in the UAE, including registration, filing procedures, tax exemptions, and strategies for minimizing tax liabilities.

Understanding Corporate Tax Laws in the UAE

Corporate tax is a significant financial consideration for businesses operating in the UAE. Introduced as part of the UAE’s commitment to aligning with international standards, corporate tax impacts both local companies and foreign entities conducting business in the region.

What is Corporate Tax in UAE?

Corporate tax in UAE is a direct tax levied on the profits of businesses. The law came into effect to diversify the country’s revenue sources beyond oil. While the UAE remains an attractive hub due to its competitive tax structure, businesses must comply with new regulations.

Who Must Register for Corporate Tax?

Businesses that generate taxable income above the exemption threshold must register with the Federal Tax Authority (FTA). Failure to comply can lead to penalties.

1. Are small businesses affected by corporate tax?

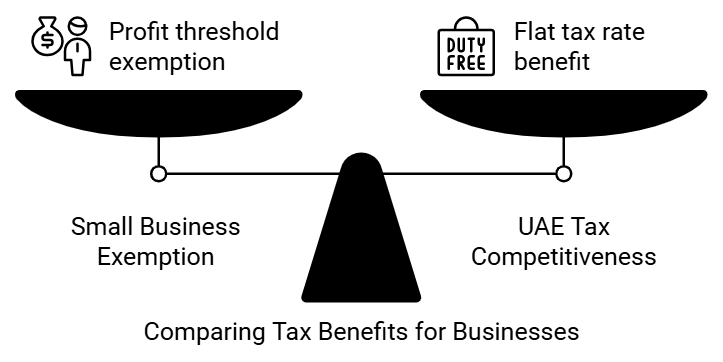

Small businesses earning less than AED 375,000 in profits are exempt from corporate tax.

2. How does the UAE compare globally in tax competitiveness?

With a flat 9% tax rate, the UAE offers one of the most business-friendly tax regimes worldwide.

The Legal Framework for Corporate Tax in UAE

The introduction of corporate tax in the United Arab Emirates represents a significant step toward aligning with global tax practices. This legal framework is designed to ensure transparency, fairness, and compliance while supporting the country’s vision for sustainable economic growth. Here’s an in-depth look at the legal structure governing corporate tax UAE.

Understanding the Corporate Tax Law

The Federal Decree-Law No. 47 of 2022 governs United Arab Emirates corporate tax. It outlines the scope, rates, exemptions, compliance requirements, and penalties for non-compliance. This law came into effect for financial years beginning on or after June 1, 2023.

Key Legal Provisions

The law’s structure provides clarity on the application of corporate tax:

| Legal Aspect | Details |

| Taxable Persons | Includes UAE-incorporated companies, branches of foreign companies, and natural persons engaged in business. |

| Exemptions | Government entities, public benefit organizations, investment funds, and qualifying free zones. |

| Tax Rates | 0% for taxable income up to AED 375,000; 9% for income above AED 375,000. |

| Qualifying Free Zone Income | Subject to 0% tax if certain conditions are met. |

| Deductible Expenses | Business expenses wholly and exclusively incurred for taxable purposes. |

| Transfer Pricing Compliance | Entities must follow arm’s length principles and maintain documentation. |

Objectives of the Legal Framework

- Economic Diversification: Reduce reliance on oil revenues by broadening the tax base.

- Global Integration: Ensure UAE tax laws align with international tax standards like the OECD’s BEPS framework.

- Compliance and Governance: Promote a transparent and well-regulated business environment.

Compliance and Registration Obligations

1. Tax Registration

All businesses subject to corporate tax must register with the Federal Tax Authority (FTA). The registration deadline varies based on the financial year-end.

2. Filing Tax Returns

Taxpayers must file their returns annually, supported by audited financial statements.

3. Documentation

Businesses must maintain detailed records of income, expenses, and tax calculations for a minimum of five years.

Penalties for Non-Compliance

The legal framework includes strict penalties to deter non-compliance:

| Type of Violation | Penalty |

| Failure to register for corporate tax | AED 10,000 (minimum), increasing with repeated offenses. |

| Failure to file tax returns on time | AED 1,000 for the first offense, escalating for delays. |

| Incorrect reporting | Penalties based on the severity and nature of the misrepresentation. |

Impact on Different Business Sectors

The legal framework ensures a level playing field across industries but considers unique sector-specific circumstances. For example:

- Real Estate: Companies involved in real estate leasing and development must evaluate income streams for taxable elements.

- SMEs: Businesses below the AED 375,000 profit threshold are exempt but must monitor income growth.

How to Stay Compliant

- Regularly review the legal requirements and updates from the FTA.

- Seek professional advice to navigate complex tax laws.

- Implement robust financial management systems to ensure accurate reporting.

Frequently Asked Questions

1. Can non-resident businesses be subject to UAE corporate tax?

Yes, non-residents earning UAE-sourced income may be taxed under the law.

2. Is corporate tax applicable to free zone companies?

Free zone companies can enjoy a 0% rate if they meet the conditions for qualifying income.

3. What happens if a business doesn’t comply?

Non-compliance can result in penalties, audits, and potential business disruptions.

UAE Corporate Tax Rates Explained

The UAE’s corporate tax regime is designed to maintain the country’s competitive edge as a business hub while meeting global taxation standards. The tax rates introduced are straightforward and aim to ease the compliance burden for businesses. This guide breaks down the UAE corporate tax rates and how they apply to various entities.

Corporate Tax Rates Overview

The corporate tax rates in the UAE are structured to support small businesses while ensuring fair taxation of larger entities:

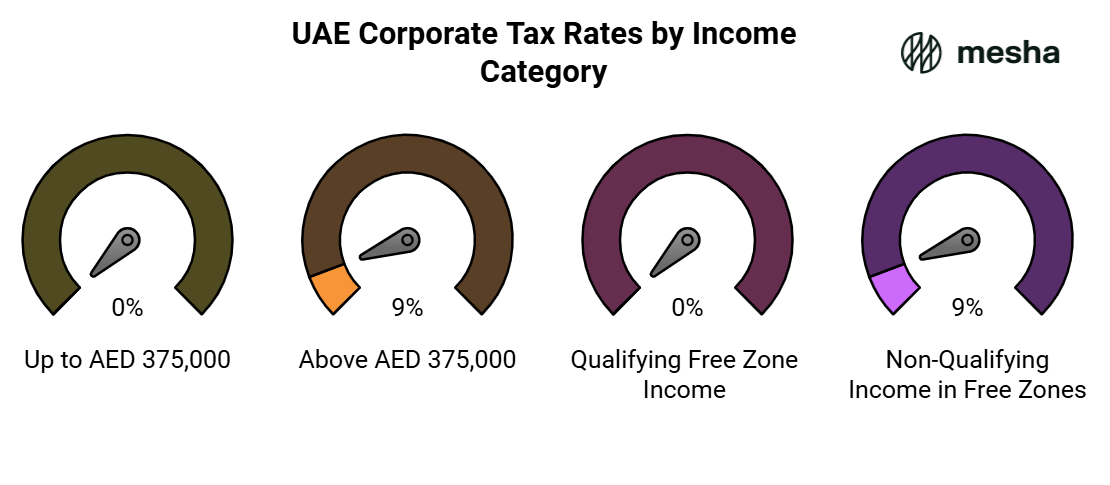

| Taxable Income | Corporate Tax Rate |

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

| Qualifying Free Zone Income | 0% (subject to meeting specific conditions) |

| Non-Qualifying Income in Free Zones | 9% |

Key Points About United Arab Emirates Corporate Tax Rates

- Small Business Support

Income below AED 375,000 is exempt from tax, allowing small businesses and startups to thrive without immediate tax pressures. - Global Competitiveness

The standard 9% rate is among the lowest in the world, making the UAE an attractive destination for multinational companies. - Free Zone Incentives

Businesses operating in free zones can enjoy a 0% tax rate on qualifying income. This maintains the UAE’s status as a hub for trade, logistics, and innovation. - Progressive Yet Simple

Unlike many countries with tiered rates, the UAE offers a flat 9% rate for taxable income above the threshold, simplifying calculations and compliance.

Examples of Corporate Tax Calculation

| Scenario | Taxable Income | Tax Rate | Tax Due |

| Small Business | AED 300,000 | 0% | AED 0 |

| Medium-Sized Enterprise | AED 500,000 | 9% on AED 125,000 | AED 11,250 |

| Large Corporation | AED 2,000,000 | 9% on AED 1,625,000 | AED 146,250 |

Note: The taxable income is calculated after deducting allowable expenses.

Checkout our corporate tax calculator for UAE

Special Cases for Tax Rates

- Free Zone Businesses

Free zone entities must adhere to specific conditions, such as conducting activities within the free zone or with foreign entities, to qualify for the 0% rate. - Multinational Corporations (MNCs)

MNCs subject to OECD’s Global Minimum Tax rules (15% for large groups) may need to pay additional taxes in their home countries. - Foreign Entities

Non-resident companies earning UAE-sourced income, such as through contracts or investments, are taxed at the 9% rate.

Comparison With Other Countries

| Country | Corporate Tax Rate | Key Notes |

| UAE | 9% | Low flat rate, free zone incentives. |

| Saudi Arabia | 20% | Higher rate for non-Saudi GCC businesses. |

| Singapore | 17% | Competitive but higher than UAE. |

| United States | 21% | Complex, with state taxes added. |

| United Kingdom | 25% (from 2023) | Higher rate to address budget deficits. |

How UAE Corporate Tax Rates Affect Businesses

- Startups: Exemption up to AED 375,000 encourages innovation and entrepreneurship.

- SMEs: The low rate allows businesses to reinvest profits and scale operations.

- MNCs: Transparent and competitive rates attract foreign direct investment.

- Free Zones: 0% rate reinforces the UAE’s position as a global trade and logistics hub.

Frequently Asked Questions

1. Are there any additional taxes beyond corporate tax?

The UAE does not impose taxes like capital gains tax or withholding tax, except for a few cases under specific conditions.

2. Do corporate tax rates differ by industry?

No, the corporate tax rates apply uniformly across all industries, except for oil and gas companies subject to separate tax frameworks.

3. Can businesses in free zones mix qualifying and non-qualifying income?

Yes, but non-qualifying income will be taxed at the standard 9% rate.

What You Need to Know About UAE Corporate Tax

The introduction of UAE corporate tax has brought significant changes to the business environment. While the country remains one of the most tax-friendly jurisdictions globally, understanding corporate tax is crucial for businesses to stay compliant and optimize their operations.

Why Was Corporate Tax Introduced in the UAE?

The UAE government implemented corporate tax to achieve several strategic objectives:

- Economic Diversification: Reduce reliance on oil revenues by creating a sustainable tax base.

- Global Standards: Align with international frameworks, such as the OECD’s Base Erosion and Profit Shifting (BEPS) project.

- Transparency: Improve reporting and compliance to attract foreign investment.

Who Is Subject to Corporate Tax?

| Category | Applicability |

| UAE-Registered Companies | Taxable on worldwide income, subject to exemptions. |

| Foreign Branches in the UAE | Taxed on UAE-sourced income only. |

| Free Zone Entities | Taxable at 0% on qualifying income; 9% on non-qualifying income. |

| Individuals Engaged in Business | Only individuals running licensed businesses are subject to corporate tax. |

| Foreign Entities | Taxed on UAE-sourced income, such as contracts or real estate investments. |

What is Taxable Income?

Taxable income is calculated as the net profit reported in the financial statements, adjusted for allowable and non-allowable expenses. Some common adjustments include:

- Allowable Deductions: Salaries, office rent, utility costs, and marketing expenses.

- Non-Allowable Deductions: Fines, personal expenses, and non-business-related costs.

How Corporate Tax Benefits the UAE Economy

- Revenue Diversification: The tax provides a stable income stream for the government.

- Improved Global Perception: Adopting corporate tax boosts the UAE’s reputation as a compliant, transparent jurisdiction.

- Business Growth: Competitive rates ensure the UAE remains a preferred destination for startups and multinational corporations.

Frequently Asked Questions

1. Are freelancers subject to corporate tax?

No, freelancers not operating under a commercial license are not subject to corporate tax.

2. Do free zone companies need to register for corporate tax?

Yes, even if they qualify for the 0% rate, free zone companies must register and file tax returns.

3. Is corporate tax applicable to all income earned by UAE businesses?

Corporate tax applies only to taxable income. Exemptions and deductions can significantly reduce the taxable base.

Step-by-Step Guide to Corporate Tax Registration in UAE

Corporate tax registration is a critical step for businesses operating in the UAE. Ensuring timely registration with the Federal Tax Authority (FTA) helps businesses comply with the law and avoid penalties. This guide provides a detailed overview of the corporate tax registration process.

Who Needs to Register for Corporate Tax?

Not all businesses are required to register immediately. The following entities must register for corporate tax:

- UAE Businesses: Companies incorporated in the UAE or operating through branches.

- Free Zone Entities: Businesses in free zones that meet the qualifying income criteria.

- Foreign Businesses: Companies earning UAE-sourced income.

- Individuals with a Business License: Individuals conducting commercial activities under a trade license.

Exempt entities such as government bodies, investment funds, and public benefit organizations do not need to register unless specified.

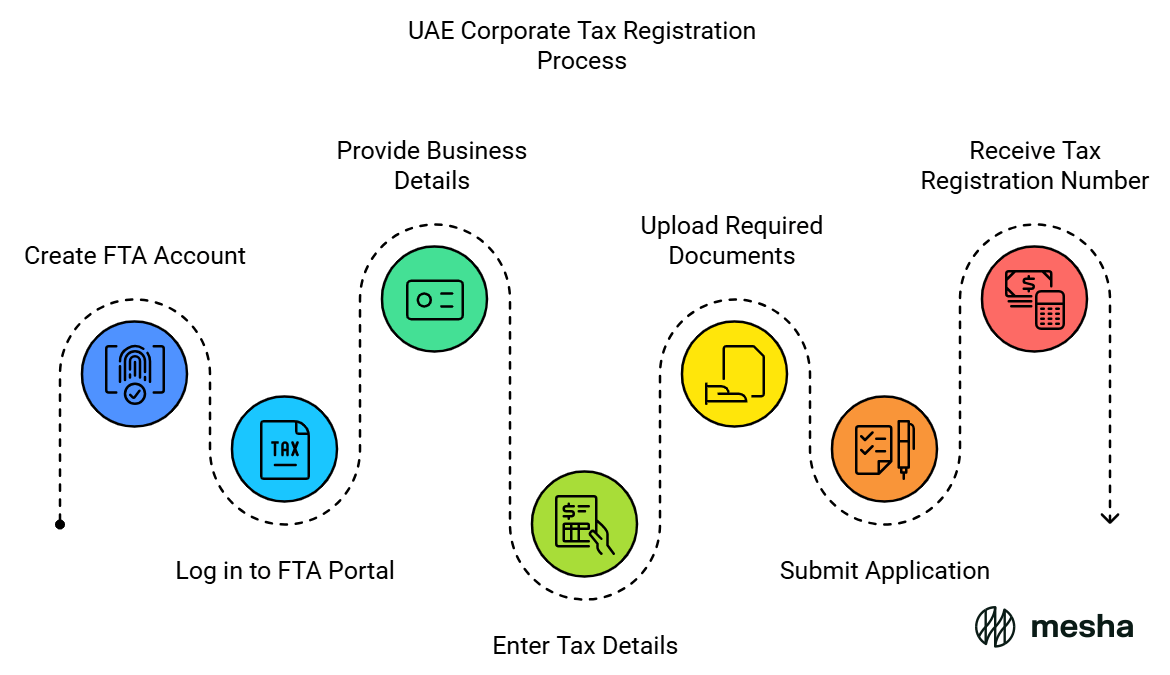

Step-by-Step Corporate Tax Registration Process

- Create an FTA Account

- Visit the Federal Tax Authority’s official website (www.tax.gov.ae).

- Create an account by providing your email address and setting up login credentials.

- Log in to the FTA Portal

Use your registered email and password to access the corporate tax registration section. - Provide Basic Business Details

- Enter the trade license details, including the license number and issuing authority.

- Provide the company’s legal name and address.

- Specify the legal structure (e.g., LLC, branch, free zone entity).

- Enter Tax Details

- Declare the financial year start and end dates.

- Indicate whether the entity qualifies for exemptions or falls under a free zone regime.

- Upload Required Documents

Ensure you have the following documents ready:- Trade license copy

- Passport and Emirates ID of owners (for individual businesses)

- Memorandum of Association (MOA) or Articles of Association (AOA)

- Proof of business activities

- Submit the Application

After completing the required fields and uploading documents, review your details and submit the application. - Receive Tax Registration Number (TRN)

Upon successful registration, you will receive a Tax Registration Number (TRN). This number must be quoted in all corporate tax filings.

Registration for Free Zone Entities

Free zone businesses must also register for corporate tax, even if they qualify for the 0% rate. These entities should ensure that their qualifying income is clearly documented to avoid complications during audits.

What Happens After Registration?

Once registered, businesses must:

- File annual corporate tax returns.

- Maintain financial records for a minimum of five years.

- Regularly check for updates or changes in tax laws on the FTA portal.

Common Mistakes to Avoid

- Late Registration: Delays can lead to penalties. Register as soon as you meet the eligibility criteria.

- Incomplete Information: Providing inaccurate or incomplete details can result in rejected applications.

- Assuming Exemption: Always confirm whether your business qualifies for exemption by reviewing the FTA guidelines.

Frequently Asked Questions

1. Is there a fee for registering for corporate tax?

No, registration with the FTA is free.

2. Can a business register before earning taxable income?

Yes, businesses are encouraged to register as soon as they meet the eligibility criteria, even if taxable income is yet to be generated.

3. Are free zone companies required to register if they qualify for 0% tax?

Yes, free zone companies must register regardless of whether their income is taxed at 0%.

Corporate Tax Exemptions in the UAE: Who Qualifies?

The UAE corporate tax regime is designed to support businesses, with specific exemptions aimed at fostering investment and economic growth. Understanding who qualifies for corporate tax exemptions is key for businesses to optimize their tax positions and remain compliant.

Entities Exempt from Corporate Tax

The UAE provides exemptions for several categories of entities. These exemptions are designed to encourage investment, support specific sectors, and maintain a favorable business environment. The main exempt entities include:

| Entity Type | Exemption Criteria |

| Government Entities | Fully exempt, as these are not engaged in commercial business operations. |

| Public Benefit Organizations | Exempt if their activities are deemed to benefit the public (subject to approval). |

| Investment Funds | Exempt if they meet specific criteria outlined by the FTA, such as being registered. |

| Pension and Social Security Funds | Exempt to ensure long-term stability for workers. |

| Charitable Organizations | Exempt if their operations are recognized as non-profit and public-oriented. |

Free Zone Entities and Their Exemption Criteria

Free zone companies are granted a 0% corporate tax rate on qualifying income. However, to benefit from this exemption, businesses must meet specific requirements set by the Federal Tax Authority (FTA):

- Conducting Activities Within the Free Zone

Free zone companies must conduct their core business activities within the designated free zone area. - Engagement in International Trade

Free zone entities that deal exclusively with foreign clients and international markets are more likely to qualify for exemptions. - Meeting FTA Compliance Criteria

To ensure transparency, businesses must adhere to FTA’s economic substance regulations. This may include maintaining adequate staff, office space, and conducting real business activities.

Income Qualifying for Exemption

Certain types of income are generally exempt from corporate tax, as long as the business meets the necessary criteria. These include:

- Income from International Trade

This applies to businesses operating in free zones or those engaged in export-oriented trade. Income generated from activities such as sales to foreign clients or international logistics can qualify for tax exemptions. - Dividend and Capital Gains Income

Income derived from the sale of shares in other companies or dividends from qualifying investments may be exempt. - Income from Government Contracts

Businesses that earn income solely from government contracts may also be eligible for tax exemptions.

How to Apply for Exemption

To apply for tax exemptions, businesses must register with the Federal Tax Authority (FTA) and provide the following documents as part of the exemption process:

- Proof of Business Activities

Companies must submit documentation proving that their activities align with the exemption criteria, such as contracts and income sources. - Tax Registration

Businesses must still register with the FTA to be officially recognized and ensure they are complying with the law. - Regular Documentation

Free zone companies and other entities seeking exemptions must maintain proper accounting records and submit financial statements to the FTA.

Corporate Tax Exemption for SMEs

Small and medium-sized enterprises (SMEs) can also benefit from specific tax relief measures under the UAE’s corporate tax laws. Businesses with taxable income up to AED 375,000 are not subject to corporate tax. This exemption allows SMEs to focus on growth without the burden of tax obligations during their initial phases of operation.

Other Notable Exemptions

- Research and Development (R&D)

Companies involved in innovation, research, and technological development may qualify for tax relief under specific government incentives aimed at encouraging scientific advancement. - Real Estate Investment

Real estate companies may qualify for exemptions if they meet the requirements for foreign investments or operate under certain conditions. This ensures the United Arab Emirates remains an attractive destination for global real estate investors. - Education and Healthcare Sectors

Businesses in the education and healthcare industries may be granted exemptions, provided they are not-for-profit or meet the regulations set by the government.

Frequently Asked Questions

1. Are all businesses in free zones exempt from corporate tax?

No, only those that meet specific criteria related to the type of income earned, and activities carried out within the free zone.

2. Can a company lose its exemption status?

Yes, a company can lose its exemption status if it fails to comply with FTA regulations or does not meet the necessary requirements for qualifying income.

3. Are real estate companies fully exempt from corporate tax?

Real estate companies may qualify for tax exemptions if they meet specific conditions related to foreign investment and business activities.

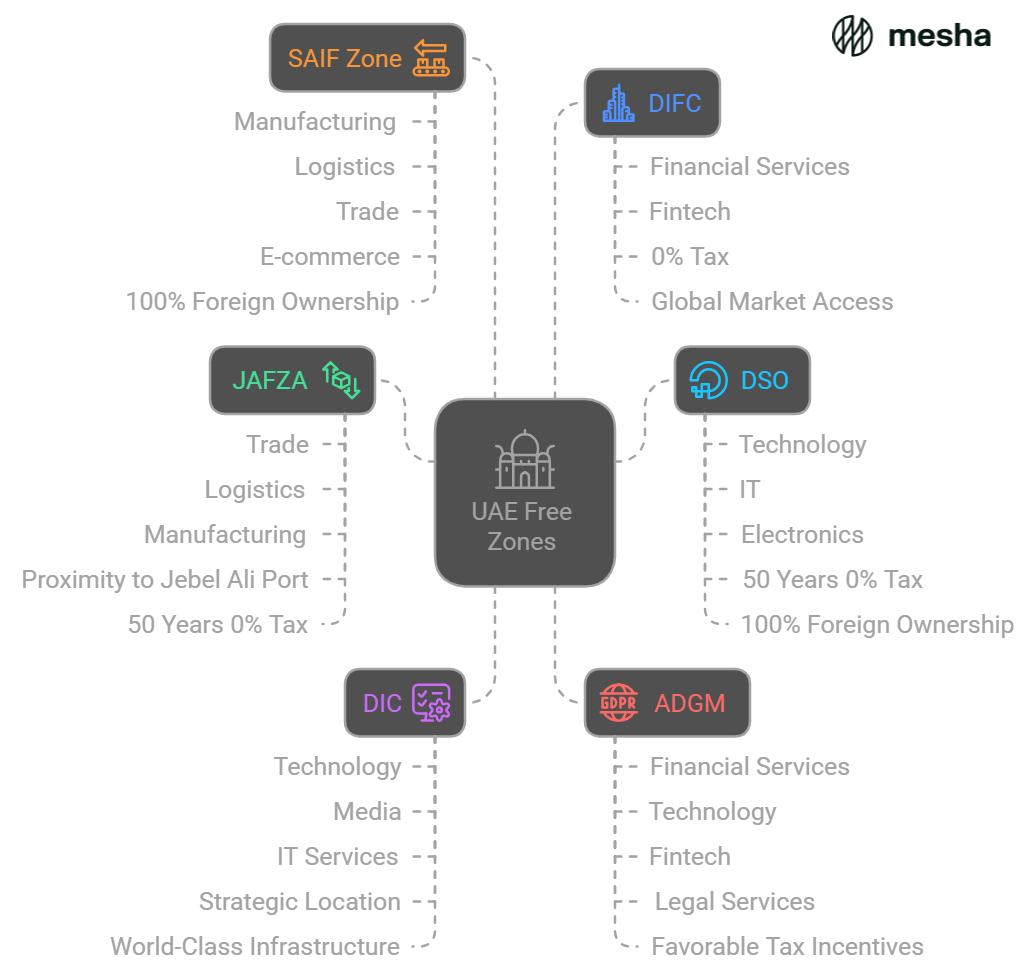

Exploring Corporate Tax-Free Zones in the UAE

The UAE has long been known for its attractive free zones, which offer various incentives to businesses, including exemptions from corporate tax. These zones are designed to foster specific industries such as technology, trade, logistics, and manufacturing, among others.

What Are Corporate Tax-Free Zones?

Corporate tax-free zones are specialized areas in the United Arab Emirates where businesses can enjoy various benefits, including exemptions from corporate tax, customs duties, and other regulatory advantages. These zones are designed to attract foreign investment and promote economic diversification by providing a favorable business environment.

Key Benefits of Corporate Tax-Free Zones

- 0% Corporate Tax

Businesses that meet the necessary criteria in free zones are exempt from corporate tax, sometimes for up to 50 years, depending on the specific free zone. - 100% Foreign Ownership

Unlike mainland companies, foreign investors in free zones can fully own their businesses without the need for a local sponsor or partner. - No Import/Export Duties

Free zone businesses enjoy exemptions from import and export duties, making it easier and more cost-effective to trade internationally. - Simplified Company Setup

Setting up a business in a free zone is typically quicker and more straightforward than in the mainland, as many free zones offer one-stop-shop services that streamline the process. - Full Repatriation of Profits

Companies can repatriate 100% of their profits and capital, providing further financial flexibility for foreign investors. - Exemption from Personal Income Tax

Free zone employees are also exempt from personal income tax, which makes it an attractive option for skilled workers and entrepreneurs.

Types of Free Zones in the UAE

The UAE hosts over 40 free zones, each catering to specific industries. Some of the most prominent ones include:

| Free Zone | Industry Focus | Key Features |

| Dubai International Financial Centre (DIFC) | Financial services, fintech | Full legal and regulatory framework, 0% tax, easy access to global markets |

| Jebel Ali Free Zone (JAFZA) | Trade, logistics, manufacturing | Proximity to Jebel Ali Port, 0% corporate tax rate for 50 years |

| Dubai Silicon Oasis (DSO) | Technology, IT, electronics | 0% corporate tax for 50 years, 100% foreign ownership |

| Dubai Internet City (DIC) | Technology, media, and IT services | Strategic location, world-class infrastructure |

| Abu Dhabi Global Market (ADGM) | Financial services, technology, fintech, legal services | Full regulatory system, favorable tax incentives |

| Sharjah Airport International Free Zone (SAIF Zone) | Manufacturing, logistics, trade, e-commerce | 0% corporate tax, 100% foreign ownership |

Free Zone Business Structure and Compliance

To enjoy the benefits of operating within a corporate tax-free zone, businesses must adhere to the rules and regulations of the specific zone. Common requirements include:

- Business Activity Restrictions

Each free zone typically has a designated list of approved activities that businesses must align with. For example, a free zone focusing on logistics may not permit manufacturing businesses. - Physical Presence Requirement

Free zone businesses must have a physical presence within the zone, such as an office or warehouse. The required space varies depending on the zone. - Economic Substance Regulations

Businesses must demonstrate real economic activity within the zone. This includes maintaining a certain number of employees and having a local office to avoid challenges during tax audits.

How to Choose the Right Free Zone

Selecting the right free zone depends on several factors, including:

- Industry Focus

Choose a free zone that caters to your industry. Some zones specialize in technology, while others focus on logistics, manufacturing, or healthcare. - Business Goals

Consider the long-term goals of your business. If you plan to expand globally, free zones with international trade links may be more suitable. - Location

The geographical location of the free zone matters. For example, zones near major ports, such as JAFZA, are ideal for logistics and shipping businesses. - Cost

Setting up and maintaining a business in a free zone comes with specific costs, such as registration fees and office space rental. Be sure to evaluate your budget before committing.

Free Zone vs. Mainland: What’s the Difference?

| Feature | Free Zone | Mainland |

| Ownership | 100% foreign ownership | 51% local ownership required |

| Tax Exemption | 0% corporate tax (up to 50 years) | Standard corporate tax applies (9%) |

| Location | Located in specific areas (not in city centers) | Can operate throughout the country |

| Business Scope | Limited to certain activities within the zone | Can do business with the entire UAE market |

| Setup Time | Faster and simpler process | More complex setup process |

Who Should Consider a Free Zone?

Free zones are best suited for businesses looking to:

- Start-Up Quickly: Free zones are ideal for startups due to their fast setup processes.

- Engage in International Trade: Businesses that deal with international customers can benefit from tax exemptions on imports and exports.

- Need 100% Foreign Ownership: Foreign entrepreneurs or investors who prefer full control over their business operations.

- Operate in Specific Industries: If your business fits within the focus of a specific free zone, you can take advantage of specialized services and infrastructure.

Essential Corporate Tax Forms for UAE Filing

Filing corporate tax returns in the UAE is an important aspect of complying with the Federal Tax Authority (FTA) regulations. Companies are required to submit several forms to ensure they meet their tax obligations correctly.

Corporate Tax Forms Overview

The UAE’s corporate tax filing system requires businesses to submit various forms depending on the type of tax and business structure. These forms help the FTA to assess the business’s tax liability and ensure compliance with the law.

Key Forms for Corporate Tax Filing

- Tax Registration Form (TRN Application)

- Purpose: Used to apply for a Tax Registration Number (TRN), which businesses must obtain before filing tax returns.

- Required Information:

- Business license details

- Company legal name and address

- Contact details for the business

- Type of business activities

- Corporate Tax Return Form (CT1)

- Purpose: The main form for submitting annual corporate tax returns.

- Required Information:

- Financial statements (Balance sheet, Profit & Loss statement)

- Income and expense details for the relevant fiscal year

- Calculation of tax due (if applicable)

- Information about any exemptions or deductions claimed

- Submission Deadline: This form must be submitted within nine months after the end of the company’s financial year.

- Declaration of Exemptions Form

- Purpose: Used to claim exemptions from corporate tax based on specific criteria such as operating in a free zone or qualifying for tax exemptions due to industry-specific rules.

- Required Information:

- Proof of exemption eligibility (e.g., Free Zone Certificate)

- Business activities and relevant income sources

- Financial statements supporting the claim

- Economic Substance Declaration

- Purpose: Required for entities that engage in certain business activities. It confirms that a business is conducting real economic activities in the UAE to meet the FTA’s economic substance requirements.

- Required Information:

- Number of employees and office location

- Details of activities conducted in the UAE

- Financial records showing the business’s physical operations

- Transfer Pricing Documentation

- Purpose: If the business is part of a multinational group, it must submit documentation related to transfer pricing rules. This ensures that intercompany transactions are conducted at arm’s length and are compliant with international tax standards.

- Required Information:

- Details of related-party transactions

- Transfer pricing policies and agreements

- Financial analysis to demonstrate arm’s length pricing

Steps for Filing Corporate Tax Forms

- Register with the FTA

- Before filing any tax returns, ensure that your business is registered with the Federal Tax Authority and has received a valid Tax Registration Number (TRN).

- Prepare Financial Statements

- Prepare the necessary financial statements for the relevant tax year. These include:

- Balance sheet

- Profit and loss statement

- Cash flow statement

- Ensure all transactions and financial activities are accurately recorded.

- Prepare the necessary financial statements for the relevant tax year. These include:

- Fill Out the Required Forms

- Complete the relevant corporate tax forms, including the Corporate Tax Return (CT1) and any other forms related to exemptions or economic substance.

- Ensure all information is accurate and complete.

- Submit the Forms Online

- Log into the FTA portal (www.tax.gov.ae) to submit the forms electronically. The FTA offers an online filing system that allows businesses to submit their forms and track their tax returns.

- Pay Tax Due (If Applicable)

- If the tax return indicates that tax is due, make the payment using the FTA’s secure online payment system. Be mindful of the payment deadlines to avoid late fees and penalties.

- Retain Copies for Record Keeping

- After filing the forms, ensure you retain copies of the submission and related documents for at least five years as required by UAE tax law.

Common Mistakes to Avoid When Filing Tax Forms

- Incomplete or Incorrect Information

- Always double-check the forms for accuracy. Mistakes in the details provided, such as incorrect income or expense figures, can lead to fines or a delay in processing.

- Missing Deadlines

- Ensure that forms are submitted on time. Missing deadlines may result in late fees or penalties. It’s advisable to submit forms ahead of time to avoid last-minute issues.

- Failure to Claim Eligible Exemptions

- Many businesses, especially those in free zones, may be eligible for corporate tax exemptions. Failing to claim these exemptions or submitting the incorrect form can lead to unnecessary tax liabilities.

- Not Providing Required Supporting Documents

- Forms like the Economic Substance Declaration or Transfer Pricing Documentation require supporting documents. Ensure these are attached to avoid delays or rejection of your submission.

Key Deadlines for UAE Corporate Tax Returns

Understanding the deadlines for submitting corporate tax returns is crucial for businesses operating in the UAE. Failing to meet these deadlines can result in penalties and legal complications.

Understanding the Tax Year in the UAE

In the UAE, the corporate tax year generally aligns with the fiscal year of the business. However, businesses can opt to have a financial year that does not necessarily coincide with the calendar year, as long as they specify this at the time of registration with the Federal Tax Authority (FTA).

Typically, companies must submit their corporate tax return within nine months from the end of their financial year. For example, if a business’s fiscal year ends on December 31, the corporate tax return would be due by September 30 of the following year.

Key Deadlines for Corporate Tax Filing

- Corporate Tax Return Filing Deadline (CT1 Form)

The main corporate tax return form (CT1) must be submitted within 9 months after the end of the company’s financial year. This means that if your financial year ends on December 31, the deadline for submitting your corporate tax return would be September 30 of the following year.

Example:- Business fiscal year ends: December 31, 2024

- Tax return filing deadline: September 30, 2025

- Economic Substance Declaration Deadline

Businesses that meet the criteria for economic substance requirements must submit an economic substance declaration. This form must be submitted within 6 months from the end of the business’s financial year.

Example:- Business fiscal year ends: December 31, 2024

- Economic substance declaration deadline: June 30, 2025

- Transfer Pricing Documentation Deadline

For companies involved in international trade or part of multinational groups, transfer pricing documentation must be submitted along with the corporate tax return. This must be submitted before the corporate tax return deadline, ensuring businesses meet compliance on intercompany pricing regulations. - VAT Filing Deadlines (if applicable)

If your business is registered for VAT, VAT returns are typically due on a quarterly or bi-monthly basis, depending on your business’s turnover and VAT registration. While VAT is separate from corporate tax, timely VAT filings are equally important to avoid penalties.

Tax Filing Reminder Tips

To help ensure that your business remains compliant, consider implementing the following practices:

- Create a Tax Calendar

Mark key deadlines for tax returns, economic substance declarations, and VAT filings on your business calendar to stay on track throughout the year. - Maintain Regular Financial Records

Keeping accurate and up-to-date financial records throughout the year ensures that you’re prepared when it’s time to file your returns. - Hire a Professional Tax Consultant

Working with a tax advisor or consultant can help ensure that your filings are correct, timely, and comply with UAE tax laws. - Automate Tax Filing Reminders

Use accounting software or tax filing platforms that send automated reminders before the submission deadlines to avoid last-minute rushes.

Special Considerations for Free Zone Businesses

Free zone businesses may have different filing deadlines depending on the nature of their activities and the specific rules of the free zone in which they operate. These businesses are also required to file corporate tax returns, even if they qualify for tax exemptions.

- Free Zone Filing Deadlines

For free zone companies, the deadlines for filing corporate tax returns typically follow the same schedule as mainland companies (i.e., within 9 months of the end of the fiscal year). However, it is important for businesses to confirm the specific rules of their free zone as some zones may have additional forms or requirements. - Exemption Documentation

Companies claiming tax exemptions (e.g., due to their activities being limited to the free zone or qualifying for specific incentives) must ensure they submit the appropriate supporting documents with their tax returns.

How UAE Corporate Tax Affects the Economy

In 2023, the UAE introduced a federal corporate tax rate of 9% for businesses that generate taxable income exceeding AED 375,000. This marked a historic change for a country that had previously operated with no corporate income tax, except for oil companies and foreign banks.

The corporate tax is part of the UAE’s efforts to modernize its tax system, generate non-oil revenues, and comply with global tax norms. However, the introduction of the corporate tax is balanced by several incentives, including exemptions for free zone businesses and provisions for tax optimization.

Impact on Businesses

- New Revenue Streams for the Government

The corporate tax system aims to provide the government with a stable and sustainable source of revenue, reducing its dependency on oil exports. This is crucial for the UAE’s long-term economic stability, particularly as the global energy market continues to evolve. - Incentive for Foreign Investment

The UAE’s tax-free zones, along with the relatively low corporate tax rate of 9%, continue to make it an attractive destination for foreign investment. The predictable tax environment, combined with other benefits such as 100% foreign ownership and repatriation of profits, helps companies maximize their returns. - Encouraging Transparency and Compliance

The introduction of corporate tax increases transparency and encourages businesses to maintain accurate financial records, ensuring a fair and compliant business environment. This move aligns the UAE with international standards for tax reporting and corporate governance. - Administrative Costs for Businesses

Businesses now need to invest in tax compliance, which includes hiring professionals or outsourcing tax services to ensure they meet the new corporate tax filing requirements. This might lead to additional administrative costs for companies, particularly small and medium-sized enterprises (SMEs).

Impact on Small and Medium-Sized Enterprises (SMEs)

For SMEs, the corporate tax system could present both challenges and opportunities:

- Challenges of Tax Compliance

While SMEs will generally be subject to the same tax rate as larger corporations, smaller businesses may find it difficult to navigate the administrative requirements associated with tax filing. Additionally, businesses with limited resources may face higher costs when seeking professional advice or setting up internal tax departments. - Opportunities for Growth

On the flip side, the introduction of corporate tax ensures a level playing field for SMEs. With large corporations also subject to taxation, SMEs may have a chance to compete more fairly in the market. Furthermore, corporate tax revenue can be reinvested in infrastructure, education, and healthcare, which may benefit SMEs indirectly by improving the business environment. - Free Zone Exemptions

Many SMEs that set up in free zones can still benefit from tax exemptions, making it easier for them to thrive while they scale their businesses. The government’s intention is to support the growth of SMEs by offering incentives for innovation and entrepreneurship in designated zones.

Impact on Key Sectors in the United Arab Emirates Economy

Several sectors of the UAE economy are directly impacted by the new corporate tax, each in different ways:

- Real Estate Sector

The UAE’s real estate sector, which has been a key driver of economic growth, is likely to see moderate changes due to corporate tax. While real estate developers will now face tax obligations, those who operate in free zones or hold long-term assets may benefit from exemptions or preferential tax rates. Additionally, the government may introduce policies to mitigate any negative effects, such as tax deductions for sustainable or green developments. - Technology and Innovation

The UAE is keen to become a hub for innovation and technology. As part of its economic diversification strategy, the government has focused on creating favorable conditions for technology companies. Tech startups in free zones are largely exempt from corporate tax for an extended period, helping them reinvest their profits into growth and innovation. - Financial Services

The financial services sector, particularly in hubs like the Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM), continues to benefit from the UAE’s pro-business tax policies. Companies in these sectors can continue to operate with favorable tax rates, including zero tax on profits for certain financial activities, allowing them to remain competitive on the global stage. - Manufacturing and Industrial Sectors

The UAE’s corporate tax system also impacts the manufacturing and industrial sectors, which are part of the government’s efforts to reduce its reliance on oil exports. These sectors can still benefit from tax incentives such as exemptions for investments in certain industries or from operating in free zones. The government’s focus on diversification is expected to drive more investment in manufacturing, which will contribute to long-term economic growth.

Impact on Global Trade and UAE’s Position in the International Market

- Attracting International Businesses

With the implementation of a low corporate tax rate, the UAE is positioning itself as a competitive business hub. The tax rate is still lower than in many other countries, making it an attractive option for multinational corporations looking to expand their operations in the Middle East. The tax system provides a stable and predictable environment for businesses engaged in global trade. - Alignment with Global Tax Standards

The introduction of corporate tax is part of the UAE’s effort to comply with international tax norms, including the OECD’s guidelines on Base Erosion and Profit Shifting (BEPS). This move ensures that the UAE remains compliant with global tax treaties and improves its standing as a financial hub in the Middle East.

Long-Term Economic Outlook

In the long run, corporate tax in the UAE is expected to drive economic diversification, attracting foreign investment, and promoting innovation. While businesses may face initial challenges in adjusting to the new tax framework, the benefits, including reinvestment in public services, infrastructure, and human capital development, are expected to outweigh the costs.

The UAE’s move toward a more diversified revenue model through corporate tax is a crucial step in ensuring sustainable economic growth and reducing dependence on oil. This will pave the way for a more resilient economy that is better equipped to face global economic challenges.

How to Save on Corporate Taxes in UAE

The UAE’s introduction of corporate tax has raised the importance of tax planning for businesses. While the corporate tax rate is relatively low at 9%, companies still need to explore strategies to minimize their tax liability legally. In this guide, we will discuss various methods businesses can use to save on corporate taxes in the UAE.

1. Take Advantage of Free Zone Exemptions

One of the most significant opportunities for businesses to save on corporate taxes in the UAE is by operating within one of the many free zones across the country. Free zones offer a range of benefits, including tax exemptions and incentives designed to attract foreign investors.

- Tax Exemptions: Companies in UAE free zones can be exempt from corporate tax for a specific period, usually 15-50 years, depending on the zone. Some zones also offer exemptions on VAT, import/export duties, and personal income taxes.

- 100% Foreign Ownership: Unlike in the mainland, businesses in free zones can be 100% foreign-owned, without the need for a UAE national partner. This is a huge advantage for international companies looking to establish a presence in the UAE.

- Eligibility for Free Zone Exemptions: To benefit from free zone exemptions, businesses must meet certain criteria, such as engaging in specific types of activities (e.g., trading, consulting, manufacturing) and ensuring they do not engage in business activities outside the free zone.

Example:

A tech company in the Dubai Silicon Oasis (DSO) could enjoy a 100% tax exemption for up to 50 years. This allows the business to reinvest profits into growth without worrying about corporate tax liabilities.

2. Leverage Tax Deductions and Credits

The UAE corporate tax law allows businesses to reduce their taxable income through various deductions and credits. By claiming eligible deductions, businesses can lower their taxable income, thus reducing their overall tax liability.

- Business Expenses: Many business-related expenses, such as operating costs, salaries, office rent, and utility bills, can be deducted from taxable income. These expenses directly contribute to the business’s operation and can significantly reduce tax liability.

- Research and Development (R&D) Costs: Companies that invest in innovation and R&D may qualify for specific tax credits or deductions. The UAE government encourages businesses to invest in technology and innovation by offering tax incentives.

- Depreciation of Assets: Depreciation of assets, such as machinery, equipment, and vehicles, can be deducted over time. This reduces the amount of taxable income, especially for businesses that rely on heavy machinery or capital-intensive assets.

Example:

A manufacturing company that buys new machinery may claim depreciation deductions on the machinery’s value, thereby lowering taxable income and saving on corporate tax.

3. Engage in Transfer Pricing

For businesses operating as part of a multinational group, transfer pricing can be a key strategy to minimize tax liabilities. Transfer pricing refers to the pricing of goods, services, and intellectual property transferred between related companies in different countries.

- Arm’s Length Pricing: The UAE’s corporate tax rules require that transactions between related entities be priced at “arm’s length” – meaning the prices charged should be similar to what would be charged between independent entities. Businesses can use this principle to structure transactions in a way that minimizes their overall tax burden.

- Transfer Pricing Documentation: To comply with international tax regulations, businesses must maintain proper transfer pricing documentation that justifies their pricing strategies. Failure to comply with these rules could result in penalties.

Example:

A UAE-based subsidiary of a multinational company may sell goods to its parent company in a lower-tax jurisdiction. By setting appropriate transfer prices, the company can allocate more profits to the UAE, where the tax rate is lower, and reduce tax exposure in higher-tax jurisdictions.

4. Consider Holding Companies

UAE businesses can set up holding companies to benefit from favorable tax policies. Holding companies are often used to manage investments in subsidiaries and other business ventures.

- Tax Benefits of Holding Companies: A holding company in the UAE may benefit from certain exemptions, such as tax exemptions on dividends and capital gains from investments in other companies. This can result in significant tax savings if the company holds investments in multiple businesses.

- Investment in Real Estate: A holding company can be used to manage real estate investments, potentially offering tax advantages such as deductions for interest payments, property expenses, and depreciation.

Example:

A UAE-based holding company with investments in several international subsidiaries can potentially reduce its taxable income by utilizing tax-efficient structures, such as exempting dividends from tax and optimizing the holding structure for capital gains tax savings.

5. Optimize Employee Compensation and Benefits

Employee compensation packages can also be structured in ways that reduce tax liability. Businesses can provide various forms of compensation that may not be subject to corporate tax, such as:

- Bonuses and Profit Sharing: Structuring employee compensation as performance-based bonuses or profit-sharing schemes can provide tax-efficient ways to pay employees, as these may be deductible expenses for the company.

- Non-Cash Benefits: Instead of cash bonuses, companies can offer non-cash benefits such as healthcare, transportation, or education allowances. These benefits may be deductible for the business and not subject to tax.

Example:

Instead of paying high cash salaries, a business could offer employees housing allowances or travel stipends, which can reduce the overall taxable income of the company.

6. Explore Double Taxation Agreements (DTAs)

The UAE has signed Double Taxation Agreements (DTAs) with numerous countries to help avoid the double taxation of income. DTAs ensure that businesses are not taxed twice on the same income – once in the country where the income is earned and again in the UAE.

- Reduced Withholding Tax: DTAs often include provisions that reduce or eliminate withholding tax on cross-border payments such as dividends, royalties, and interest.

- Tax Credits for Foreign Taxes Paid: If a business pays taxes in a foreign jurisdiction, it may be able to claim a credit against its UAE tax liability, reducing the amount of tax owed in the UAE.

Example:

A UAE-based company earning income from a European subsidiary may be able to claim a reduced withholding tax rate on royalties or dividends, thanks to a DTA between the UAE and the relevant European country.

7. Reinvest Profits for Tax Optimization

Reinvesting profits into the business is one of the simplest ways to reduce taxable income. The UAE tax system allows businesses to reinvest profits into expansion, R&D, or other capital expenditures without facing immediate tax implications.

- Reinvestment in Assets: Purchasing new equipment, technology, or expanding operations can reduce taxable income by increasing allowable deductions.

- Investing in Innovation: Businesses can reinvest profits in research, product development, and innovation, which may qualify for tax credits or deductions, further reducing their overall tax burden.

Example:

A company that reinvests profits into developing a new product line or opening a new branch may qualify for deductions related to those investments, reducing their taxable income.

Corporate Tax Penalties in the UAE: Avoid Costly Mistakes

The UAE has a strict framework for ensuring compliance with corporate tax laws. Under the Federal Tax Authority (FTA), businesses are required to file their corporate tax returns on time, pay taxes owed, and maintain accurate financial records. Failure to meet these requirements can result in substantial penalties.

The penalties can be imposed for various reasons, including late filings, incorrect filings, failure to pay taxes, and non-compliance with other tax regulations. The goal of these penalties is to encourage businesses to adhere to tax laws and promote transparency and fairness within the tax system.

Types of Penalties Businesses Can Face

- Late Filing Penalties

One of the most common penalties businesses face is the fine for late submission of corporate tax returns. Companies are required to file their tax returns within 9 months after the end of their financial year. If they miss this deadline, they will be subject to penalties.

| Violation | Penalty |

| Late submission of corporate tax return | AED 10,000 for the first offense, AED 20,000 for subsequent offenses |

- Failure to Pay Taxes on Time

If a business fails to pay its corporate tax on time, it will incur penalties in addition to the unpaid tax. The UAE tax system requires that taxes be paid within the filing deadline.

| Violation | Penalty |

| Failure to pay taxes on time | Interest of 1% per month on the outstanding tax amount |

| Plus an additional 4% penalty if payment is delayed by more than 20 days |

- Inaccurate or Incorrect Filings

Submitting inaccurate or incomplete corporate tax returns can lead to hefty penalties. If the FTA determines that a business has intentionally underreported its income or inflated its expenses, this can lead to criminal charges, fines, and potentially even the suspension of operations.

| Violation | Penalty |

| Inaccurate or false tax returns | Fines up to AED 50,000, or higher, depending on the severity of the violation |

- Failure to Maintain Adequate Financial Records

Businesses are required to maintain proper accounting records to support their corporate tax filings. Failing to maintain accurate records can lead to penalties and additional scrutiny from tax authorities.

| Violation | Penalty |

| Failure to maintain adequate financial records | AED 10,000 for the first offense, AED 20,000 for subsequent offenses |

- Failure to Submit Economic Substance Declaration

Companies that fall under the Economic Substance Regulations must submit an economic substance declaration along with their corporate tax returns. If a company fails to meet this requirement, they could face penalties.

| Violation | Penalty |

| Failure to submit economic substance declaration | AED 20,000 for the first year, AED 50,000 for subsequent years |

How to Avoid Corporate Tax Penalties in the UAE

- Stay Organized and Maintain Proper Records

One of the most effective ways to avoid penalties is by maintaining accurate and up-to-date financial records. This includes keeping detailed accounts of all income, expenses, assets, and liabilities. Proper record-keeping ensures that businesses are ready for any tax audits and can submit accurate tax returns.

- Tip: Use accounting software or hire a professional accountant to ensure your records are comprehensive and comply with tax laws.

- File Corporate Tax Returns on Time

Timely filing of tax returns is crucial to avoid late submission penalties. Remember, businesses must file their tax returns within 9 months of the end of their fiscal year. Set reminders in advance to ensure that all forms are submitted on time.

- Tip: Create a tax calendar with all key deadlines and automate reminders to avoid missing the filing dates.

- Ensure Accuracy in Your Tax Returns

Double-check all figures and calculations when preparing your corporate tax return. Inaccurate reporting can lead to fines or more severe penalties. If you’re unsure about any figures or deductions, consult with a tax advisor.

- Tip: Seek professional help or hire a tax consultant if you have doubts about your tax calculations or filings.

- Pay Taxes Promptly

Ensure that your business pays any corporate tax liabilities on time. Late payments can lead to interest charges, and if payments are delayed for more than 20 days, additional penalties will apply.

- Tip: Set up automated payments or establish a dedicated tax account to ensure taxes are paid on time.

- Stay Updated on Tax Laws and Regulations

The UAE’s tax regulations are evolving, and it’s crucial for businesses to stay informed about any changes to corporate tax laws. This includes understanding any new exemptions, deductions, or amendments to filing procedures.

- Tip: Subscribe to updates from the UAE Federal Tax Authority or work with a tax advisor to stay on top of regulatory changes.

- Submit Economic Substance Declarations on Time

Companies that are subject to the Economic Substance Regulations must submit the required economic substance declaration. Failing to do so will result in penalties.

- Tip: Review whether your business activities fall under these regulations and ensure timely submission of the required forms.

What to Do If You Receive a Penalty

If your business receives a penalty, it’s essential to act quickly:

- Review the Notice: Carefully review the penalty notice from the FTA to understand why the penalty was imposed.

- File an Appeal: If you believe the penalty was issued in error, you have the right to appeal. The FTA allows businesses to challenge penalties within a specific time frame.

- Pay the Penalty: If the penalty is valid, make sure to pay it promptly to avoid additional charges or further enforcement actions.

- Implement Preventative Measures: To avoid future penalties, consider revising your tax practices and ensuring that all filings and payments are made correctly and on time.

Corporate Tax Audits: What to Expect

A corporate tax audit is an examination of a company’s financial records and transactions by the UAE’s Federal Tax Authority (FTA). The goal of the audit is to ensure that businesses are complying with corporate tax laws, including filing tax returns accurately, paying the correct amount of tax, and maintaining the necessary documentation.

The FTA has the authority to audit any company subject to corporate tax, and audits can be triggered for various reasons, such as random selection, discrepancies in tax filings, or suspicious activities. The FTA’s main aim is to ensure that businesses are paying their fair share of taxes and adhering to tax regulations.

Reasons for a Corporate Tax Audit

While tax audits in the UAE are not always anticipated, there are several reasons why a business might be selected for an audit. These include:

- Discrepancies in Tax Filings: If the information on a company’s tax returns doesn’t align with their financial records or previous filings, it can raise red flags. This could include underreporting income, overreporting expenses, or claiming ineligible deductions.

- Failure to File Returns on Time: Companies that have a history of late filings or non-compliance with tax deadlines may be subject to an audit. Late payments of taxes or inconsistent tax filings can signal that a business might not be adhering to proper tax regulations.

- Random Selection: Just like in many other jurisdictions, businesses can be selected for an audit randomly. This is part of the FTA’s strategy to ensure all businesses are complying with tax regulations.

- Suspicious Transactions or Patterns: If a business engages in transactions that appear unusual or suspicious—such as large transfers or complex financial arrangements—the FTA may initiate an audit to investigate further.

- Economic Substance Violations: Businesses that are required to adhere to the Economic Substance Regulations may be audited to ensure they meet the requirements for economic substance. Failing to meet these regulations can lead to penalties, including the imposition of fines.

What Happens During a Corporate Tax Audit?

A corporate tax audit typically involves the FTA reviewing your business’s financial records and tax filings. Below is an overview of what to expect during the audit process:

- Notification of the Audit: The FTA will notify the company in writing that an audit is being conducted. This notification will include the reason for the audit, the scope, and the period under review. In some cases, the audit may focus on a specific issue, while in others, it may cover the entire tax history of the company.

- Document Review: During the audit, the FTA will examine a company’s accounting records, tax filings, financial statements, and any supporting documents such as invoices, contracts, receipts, and bank statements. The FTA may also review the company’s corporate structure, related-party transactions, and transfer pricing arrangements.

- Interviews and Clarifications: The FTA may request interviews or meetings with the company’s management, accountants, or tax advisors to clarify specific transactions or financial practices. It’s essential to be cooperative and transparent during this process.

- Assessment of Tax Liabilities: If the FTA finds any discrepancies or areas of non-compliance during the audit, they will assess additional taxes, penalties, and interest charges. Businesses may also be required to correct their filings and pay the outstanding tax amounts.

- Audit Report and Conclusion: After the audit is completed, the FTA will issue a report detailing the findings, including any tax discrepancies, errors, or violations discovered. The company will have the opportunity to review the report and discuss any disagreements with the FTA.

Potential Outcomes of a Corporate Tax Audit

There are several potential outcomes after a corporate tax audit, depending on the findings:

- No Changes or Penalties: If the audit finds that the company has complied with tax laws and regulations, the audit will close without any changes. This outcome is the best-case scenario for businesses.

- Additional Taxes Owed: If the FTA identifies underreported income or ineligible deductions, the company may be required to pay additional taxes, along with any penalties or interest charges for late payments.

- Penalties for Non-Compliance: If the audit uncovers significant violations, such as deliberate underreporting of income or tax evasion, the company could face penalties. Penalties for serious non-compliance can range from fines to criminal charges, depending on the severity of the violation.

- Tax Adjustments: In some cases, the FTA may adjust a company’s tax filings to ensure that the taxes owed are correct. This could include recalculating income, deductions, or tax credits based on the audit findings.

How to Prepare for a Corporate Tax Audit

Being proactive and prepared for a corporate tax audit can help businesses avoid complications and penalties. Here are a few steps to ensure a smooth audit process:

- Maintain Accurate and Organized Records: Keeping detailed and up-to-date financial records is the first line of defense against an audit. Make sure all transactions are well-documented, and keep all supporting documents such as receipts, contracts, and invoices.

- Understand Tax Filing Requirements: Ensure that your company fully understands and complies with UAE tax filing requirements. This includes adhering to deadlines, correctly reporting income and expenses, and understanding tax laws relevant to your business.

- Consult with Tax Experts: If your company faces a complex audit, it’s advisable to consult with tax professionals or advisors who are well-versed in UAE tax laws. They can help you navigate the audit process, respond to FTA inquiries, and represent your company during any discussions or negotiations.

- Perform Internal Audits: Conduct regular internal audits to ensure your records and tax filings are accurate. An internal audit can help you identify potential issues before the FTA comes to review your tax returns.

- Respond Promptly to Audit Requests: If the FTA requests specific documents or clarifications, respond promptly and provide the necessary information. Cooperation can lead to a more favorable outcome.

What to Do If Your Business is Audited

If your business is selected for a tax audit, here are some important steps to follow:

- Review the Audit Notice: Carefully read the audit notice to understand the scope and nature of the audit. This will help you prepare the necessary documents.

- Gather Required Documentation: Collect all the requested financial records and tax filings. Be prepared to provide any supporting documents that may be needed, including bank statements, invoices, and contracts.

- Consult with Experts: Engage a tax consultant or legal advisor to guide you through the audit process. They can help you prepare for meetings, ensure compliance with tax laws, and represent your business if disputes arise.

- Address Any Issues Found: If the audit uncovers any discrepancies or errors, work with the FTA to resolve the issues as soon as possible. This could involve correcting filings, paying additional taxes, or addressing any compliance failures.

Key Corporate Tax Treaties in the UAE

A corporate tax treaty is an agreement between two countries that aims to avoid double taxation on income earned by a company operating in both jurisdictions. These treaties are essential for businesses that operate internationally, as they help determine which country has taxing rights over various types of income, such as dividends, interest, royalties, and business profits.

The main objectives of corporate tax treaties include:

- Eliminating Double Taxation: Treaties ensure that businesses are not taxed twice on the same income—once in the country where the income is generated and again in the country of residence of the business.

- Reducing Tax Rates: Tax treaties often provide reduced withholding tax rates on dividends, interest, and royalties, which can lower the overall tax burden for companies operating internationally.

- Providing Tax Certainty: Tax treaties help provide clarity on tax obligations, reducing the risk of disputes between businesses and tax authorities.

UAE’s Network of Tax Treaties

As part of its efforts to integrate into the global economy and attract international investors, the UAE has signed numerous tax treaties with other countries. The UAE has a network of over 130 double tax treaties (DTTs) with countries across the globe. These treaties cover a wide range of tax matters and help reduce the burden of taxation on businesses and investors.

The UAE’s tax treaty network includes agreements with major economies such as:

- United Kingdom

- United States

- India

- China

- Germany

- France

- Japan

- Singapore

- Saudi Arabia

These treaties are important for businesses in the UAE, as they provide various tax advantages for companies doing business internationally.

Benefits of Corporate Tax Treaties for UAE Businesses

- Avoidance of Double Taxation

One of the primary benefits of corporate tax treaties is the prevention of double taxation. Without a tax treaty, a company that earns income in another country may be taxed by both that country and the UAE, resulting in double taxation. A tax treaty allocates taxing rights between the two countries, ensuring that businesses are only taxed once on income generated abroad.

For example, if a UAE-based company receives dividends from a subsidiary in the United Kingdom, the income may be subject to withholding tax in the UK. However, under the UAE-UK tax treaty, the UAE business may be eligible for a reduced withholding tax rate, or even a complete exemption from UK tax on dividends.

- Reduced Withholding Tax Rates

Corporate tax treaties often reduce or eliminate withholding taxes on income such as dividends, interest, and royalties. This can result in significant tax savings for companies engaged in cross-border transactions.

| Income Type | Typical Tax Rate without Treaty | Typical Tax Rate under UAE Treaty |

| Dividends | 10% – 30% | 5% – 10% |

| Interest | 15% | 5% – 10% |

| Royalties | 15% | 5% – 10% |

These reduced tax rates can significantly lower the overall cost of doing business and increase profitability for UAE-based companies with international operations.

- Clarity and Certainty

Tax treaties provide clear guidelines on which country has the right to tax certain types of income. This reduces the risk of tax disputes between businesses and tax authorities and offers a level of tax certainty for companies operating internationally.

- Tax Relief for Expatriates and Foreign Investors

Corporate tax treaties can also benefit expatriates and foreign investors working in the UAE. Many treaties contain provisions that help expatriates avoid double taxation on income earned both in their home country and in the UAE. Additionally, tax treaties often reduce the tax burden on foreign investors by offering exemptions or reductions on capital gains tax.

Notable UAE Corporate Tax Treaties

Let’s take a closer look at some of the most important corporate tax treaties that the UAE has signed with other countries:

UAE-United States Tax Treaty

The UAE and the United States signed a double tax treaty (DTT) to avoid double taxation and to facilitate trade and investment between the two countries. Key benefits of the UAE-US treaty include:

- Exemption of Dividends: Dividends paid by a UAE company to a US investor are typically exempt from UAE withholding tax, and the tax rate on dividends in the US is reduced under the treaty.

- Reduced Withholding Taxes on Royalties: The treaty provides a reduced withholding tax rate on royalties paid to US companies.

- Tax Credits for US Residents: US residents who pay tax in the UAE can often claim tax credits to offset US tax liabilities.

UAE-India Tax Treaty

The UAE and India have a comprehensive tax treaty that covers various aspects of taxation, including income tax, business profits, and capital gains. Key benefits of the UAE-India treaty include:

- Lower Withholding Taxes: The treaty reduces the withholding tax on dividends, interest, and royalties, benefiting businesses engaged in cross-border transactions between the two countries.

- Exemption from Capital Gains Tax: The treaty ensures that UAE-based companies are not subject to capital gains tax when selling shares in Indian companies, provided certain conditions are met.

- Tax Residency Benefits: The treaty includes provisions that help determine tax residency, preventing both India and the UAE from taxing the same income.

UAE-Singapore Tax Treaty

Singapore and the UAE have a tax treaty that offers several tax benefits to businesses. These benefits include:

- Exemption on Dividends: Dividends paid between Singapore and UAE companies are generally exempt from withholding tax under the treaty.

- Reduced Rates on Interest and Royalties: The treaty reduces withholding tax rates on interest and royalties between the two countries, which is particularly beneficial for businesses in the finance, technology, and intellectual property sectors.

How to Utilize Tax Treaties Effectively

- Understand Treaty Provisions

Companies should thoroughly review the provisions of the relevant tax treaties to understand the benefits available to them. This includes understanding the withholding tax rates, exemptions, and any other tax relief available under the treaties.

- Keep Accurate Records

To benefit from tax treaty provisions, businesses must maintain accurate and up-to-date records of their transactions with foreign entities. This includes keeping track of income earned, tax paid, and any required forms or certificates related to the treaty benefits.

- Consult with Tax Experts

Navigating the complexities of international tax treaties can be challenging. It’s advisable for businesses to consult with tax advisors or consultants who specialize in UAE tax law and international tax treaties. These professionals can help ensure that businesses are maximizing the benefits available under tax treaties and complying with all relevant regulations.

Key Corporate Tax Treaties in the UAE

The UAE has established itself as a global business hub, thanks in part to its extensive network of Double Taxation Avoidance Agreements (DTAs) and other corporate tax treaties. These agreements aim to eliminate double taxation, foster international trade, and attract foreign investment.

What are Corporate Tax Treaties?

Corporate tax treaties are agreements between two countries to reduce or eliminate taxation on income earned across borders. They:

- Prevent double taxation on profits.

- Provide tax relief for companies operating internationally.

- Encourage global business activities.

Overview of UAE’s Tax Treaties

As of 2024, the UAE has signed DTAs with 137 countries, including major trading partners like:

- India

- United States

- United Kingdom

- Germany

- China

How Businesses Can Leverage UAE Tax Treaties

- Choose the Right Entity Type: Multinational companies can optimize taxes by selecting UAE-based entities like Free Zone companies or mainland LLCs.

- Use Treaty Benefits for Expansion: Businesses expanding to treaty countries can negotiate better terms using reduced tax rates.

- Plan Tax Residency Strategically: Maintaining UAE tax residency ensures full access to treaty benefits.

Corporate Tax Registration Requirements in UAE

In the UAE, businesses need to understand the mandatory registration requirements to comply with the country’s tax regulations. Registration is crucial to avoid penalties and maintain smooth operations.

Who Needs to Register for Corporate Tax in UAE?

All businesses operating in the UAE are generally required to register for corporate tax, except those explicitly exempted. Here’s a breakdown:

| Category | Registration Requirement |

| UAE Mainland Companies | Must register, regardless of size or sector. |

| Free Zone Companies | Must register, even if benefiting from a 0% tax rate. |

| Government and Government-Owned Entities | Exempt, unless involved in commercial activities. |

| Small Businesses (Below AED 375,000 Turnover) | Must register but can qualify for a 0% tax rate. |

| Natural Resource Extraction Companies | Exempt under certain conditions. |

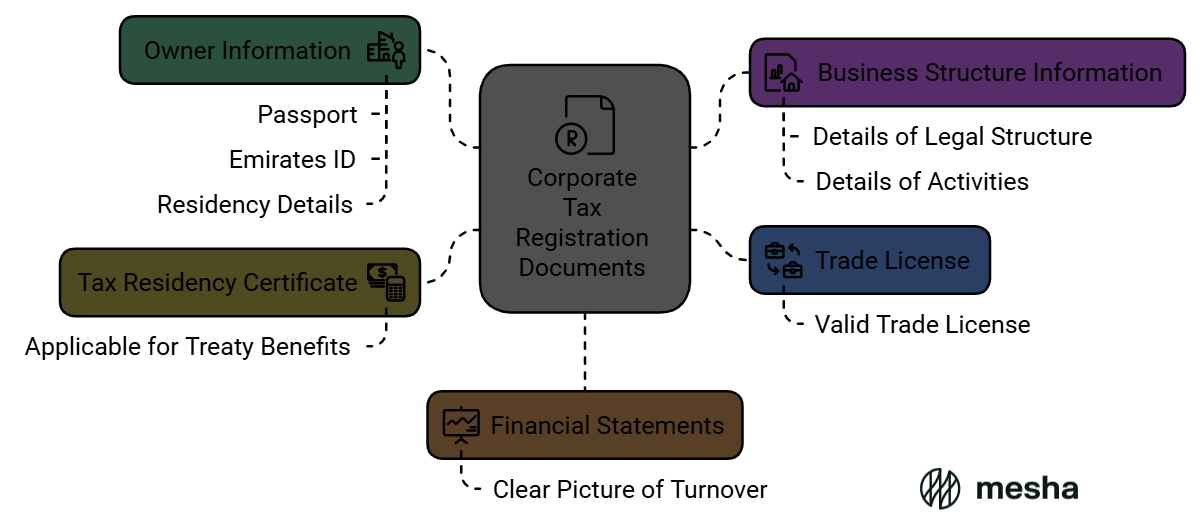

Documents Required for Corporate Tax Registration

To register successfully, businesses must prepare the following documents:

- Trade License: A copy of the valid trade license.

- Owner Information: Passport, Emirates ID, and residency details for all shareholders or partners.

- Tax Residency Certificate (if applicable): For businesses claiming treaty benefits.

- Financial Statements: For a clear picture of the company’s turnover.

- Business Structure Information: Details of legal structure and activities.

Registration Timeline

Corporate tax registration must be completed well before the first corporate tax filing deadline. Early registration ensures compliance and avoids unnecessary penalties.

Steps to Register for Corporate Tax in UAE

- Create an Account:

Visit the Federal Tax Authority (FTA) website and create a user account. - Provide Business Details:

Enter company details, including trade license number, legal structure, and address. - Upload Documents:

Submit all required documents in digital format. - Verify Information:

Cross-check the details before submitting the application to avoid delays. - Receive Tax Registration Number (TRN):

Once approved, the FTA will issue a unique TRN, confirming your registration.

Exemptions from Registration

Certain entities may be exempt from registering for corporate tax:

- Businesses engaged in natural resource extraction (subject to emirate-level taxation).

- Entities operating within qualifying Free Zones under specific conditions.

Potential Penalties for Non-Compliance

Failing to register for corporate tax can lead to financial and legal repercussions, such as:

- Fines starting from AED 10,000 for non-registration.

- Additional penalties for non-payment or late filing.

Pro-Tip for Businesses

Even if your business qualifies for a 0% corporate tax rate, you are still obligated to register. Keeping proper financial records is essential for future audits or inquiries.

Step-by-Step Guide to Corporate Tax Registration in UAE

Registering for corporate tax in the UAE is a straightforward process when approached systematically. This guide will help businesses navigate each step of the process to ensure compliance with the Federal Tax Authority (FTA) requirements.

Why is Corporate Tax Registration Important?

Corporate tax registration is mandatory for businesses to:

- Fulfill UAE tax law obligations.

- Obtain a Tax Registration Number (TRN) for filing returns.

- Avoid penalties for non-compliance.

Step-by-Step Guide to Register for Corporate Tax

- Prepare the Required Documents

Before beginning the registration process, gather all the necessary documentation:- Trade License: To verify business activities.

- Owner Information: Passport and Emirates ID for all shareholders or partners.

- Business Structure Details: Legal form, address, and ownership details.

- Financial Records: Proof of turnover to determine eligibility for exemptions or reduced rates.

- Create an Account on the FTA Portal

- Visit the Federal Tax Authority’s website.

- Click on “Sign Up” to create an account.

- Provide your email, create a secure password, and verify your account.

- Log In and Access the Corporate Tax Registration Form

- After logging in, navigate to the “Corporate Tax” section on the dashboard.

- Select “Register for Corporate Tax” to access the form.

- Complete the Registration Form

- Business Information: Include trade license number, legal structure, and business type (mainland, free zone, etc.).

- Contact Information: Provide accurate details for communication purposes.

- Owner Details: Enter shareholder or partner information as required.

- Upload Supporting Documents

- Use the upload feature to submit the scanned copies of your trade license, financial records, and ownership documents.

- Review and Submit

- Double-check all entries to ensure accuracy.

- Submit the application and wait for confirmation from the FTA.

- Receive the Tax Registration Number (TRN)

- Upon approval, the FTA will issue a TRN, which serves as your corporate tax identifier.

Example: Corporate Tax Registration Timeline

| Step | Timeline |

| Document Preparation | 1-3 business days |

| Account Creation on FTA Portal | Immediate |

| Form Submission | 1-2 hours |

| FTA Approval and TRN Issuance | 5-10 business days |

What Happens After Registration?

Once registered, businesses must:

- Keep the TRN handy for filing corporate tax returns.