Complete guide to Rental income and taxes 2024

Rental income can be a lucrative source of revenue for small business owners in the United States, but navigating the complex landscape of taxes is crucial for optimizing returns and avoiding potential pitfalls.

In this comprehensive guide, we will delve into the intricacies of rental income taxation, providing small business owners with valuable insights to make informed decisions.

In this blog we’ll discuss:

- Types of rental income

- Tax Deductions for Rental Properties

- Forms to fill out for rental deduction

- Section 199A Deduction for QBI

Types of Rental Income

A. Differentiating between Rent, Lease Payments, and Additional Fees:

- Rent:

- Description:

- Regular payments are made by tenants to the property owner for the use and occupancy of the property.

- Key Points:

- Usually paid monthly.

- Considered a fundamental component of rental income.

- Description:

- Lease Payments:

- Description:

- Payments are made under a lease agreement, which may include rent as well as additional charges for specific services or amenities.

- Key Points:

- Can encompass a broader range of charges beyond basic rent.

- This often applies to commercial leases where tenants may pay for utilities, maintenance, or other services.

- Description:

- Additional Fees:

- Description:

- Extra charges beyond the standard rent or lease payments, such as fees for late payments, parking, or pet rent.

- Key Points:

- Should be clearly outlined in the lease agreement.

- Can provide additional income for property owners beyond the standard rent.

- Description:

B. Overview of Residential, Commercial, and Vacation Rental Properties:

- Residential Rental Properties:

- Description:

- Properties leased or rented for individuals or families to use as their primary residence.

- Key Points:

- Typically subject to residential lease agreements.

- Rent is generally paid monthly.

- Common types include single-family homes, apartments, and condominiums.

- Description:

- Commercial Rental Properties:

- Description:

- Properties leased to businesses for commercial purposes, such as office spaces, retail shops, or industrial facilities.

- Key Points:

- Lease terms are often longer than residential leases.

- Lease payments may include additional charges for maintenance, utilities, or property improvements.

- Lease agreements may have more complex terms and conditions.

- Description:

- Vacation Rental Properties:

- Description:

- Properties are rented on a short-term basis for vacation or temporary stays.

- Key Points:

- Rent is often charged on a nightly or weekly basis.

- Popular through online platforms like Airbnb or VRBO.

- Additional fees may include cleaning fees, security deposits, or fees for specific amenities.

- Description:

- Considerations for Property Owners:

- Each type of rental property comes with its unique challenges and opportunities.

- Property owners should be aware of local regulations, zoning laws, and market dynamics specific to the type of rental property.

- Marketing and management strategies may vary based on the target tenant or guest demographic.

Understanding the nuances of different types of rental income is crucial for property owners to effectively manage their properties, set appropriate rental rates, and maximize overall rental income. It’s also important to stay informed about local and state regulations that may impact rental arrangements.

Tax Deductions for Rental Properties

Tax deductions for rental properties can help property owners reduce their taxable income. Here are some common deductions associated with rental properties:

A. Mortgage Interest Deduction:

- Description:

- Allows property owners to deduct interest payments made on the mortgage used to acquire, improve, or build the rental property.

- Key Points:

- Limited to the interest portion of mortgage payments.

- Applicable to mortgages secured by the rental property.

- Deductions may be subject to limitations for higher-income taxpayers.

B. Property Tax Deduction:

- Description:

- Permits property owners to deduct the property taxes paid on their rental properties.

- Key Points:

- Deductible taxes include those assessed on the property’s assessed value.

- Special assessments for local improvements may also qualify.

C. Insurance and Maintenance Cost Deductions:

- Description:

- Allows the deduction of costs related to maintaining and insuring the rental property.

- Key Points:

- Repairs and maintenance costs must be necessary to keep the property in good working condition.

- Deductible insurance includes premiums for property, liability, and landlord-specific policies.

D. Depreciation as a Deductible Expense:

- Description:

- Permits property owners to recover the cost of the property over time.

- Key Points:

- Residential properties are typically depreciated over 27.5 years; commercial properties over 39 years.

- The depreciable basis is the property’s total cost minus the value of the land.

- Annual depreciation is claimed on tax returns.

E. Other Deductible Expenses:

- Description:

- Beyond the major categories, there are various other deductible expenses.

- Key Points:

- Advertising and marketing costs for finding tenants.

- Legal and professional fees related to the property (e.g., legal advice, property management fees).

- Utilities and operating expenses are directly associated with the rental property.

- Travel expenses for property-related activities (e.g., visiting the property for maintenance).

F. Record-Keeping and Documentation:

- Description:

- Proper documentation is crucial for supporting deductions during tax filing.

- Key Points:

- Maintain organized records of all expenses, including receipts, invoices, and contracts.

- Keep a separate bank account for rental property transactions to streamline record-keeping.

- Utilize accounting software or hire a professional accountant to ensure accuracy.

Forms to fill out for rental deduction

When reporting rental income for tax purposes in the United States, there are specific forms that individuals, including small business owners, typically use. The primary form for reporting rental income and expenses is Schedule E (Form 1040), Supplemental Income and Loss. Here’s a breakdown of the relevant forms and their purposes:

- Schedule E (Form 1040): Supplemental Income and Loss:

- Purpose: Schedule E is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs (Real Estate Mortgage Investment Conduits).

- Details: You’ll provide information about your rental income, deductible expenses, and depreciation on this form.

- Form 1040 (U.S. Individual Income Tax Return):

- Purpose: The main individual tax return form where you report your total income, including rental income reported on Schedule E

- Details: You’ll transfer the net income or loss from Schedule E to your Form 1040.

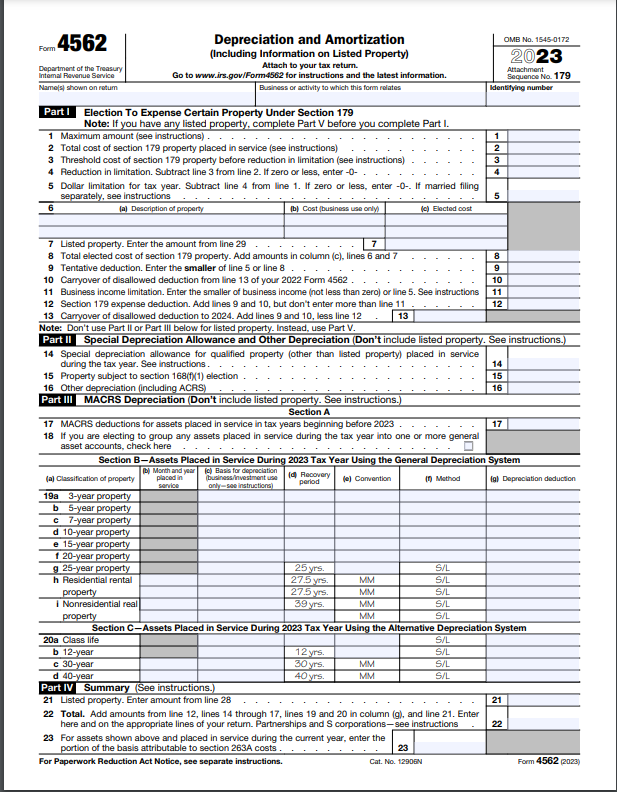

- Form 4562 (Depreciation and Amortization):

- Purpose: If you claim depreciation on your rental property, Form 4562 is used to report and calculate the depreciation deduction.

- Details: Provide information about the property, its cost, and the depreciation method used.

- Form 8825 (Rental Real Estate Income and Expenses of a Partnership or an S Corporation):

- Purpose: If you own rental property through a partnership or an S corporation, this form is used to report the income and expenses associated with the rental property.

- Details: Partnerships and S corporations report rental activities at the entity level, and this information flows through to the individual owners.

- Form 8582 (Passive Activity Loss Limitations):

- Purpose: If you have passive activity losses, such as from rental activities, Form 8582 is used to calculate and report limitations on these losses.

- Details: This form helps determine if your losses can be fully deducted or if they are subject to limitations.

Remember, the specific forms you use may vary based on your individual circumstances, such as the type of property you own, how you own it (individually or through an entity), and whether you actively participate in managing the rental

Section 199A Deduction for QBI

Section 199A of the Internal Revenue Code, introduced by the Tax Cuts and Jobs Act (TCJA) in 2017, provides a deduction for qualified business income (QBI) for pass-through entities, such as sole proprietorships, partnerships, and S corporations. The deduction is designed to provide tax relief to small business owners, including those who generate income through rental activities.

- Pass-Through Entities: Section 199A primarily benefits individuals and entities that do not pay income tax at the entity level but instead pass income through to their owners or shareholders.

- QBI Definition: Qualified Business Income (QBI) encompasses income, gains, deductions, and losses from a qualified trade or business. Certain types of income, such as capital gains and dividends, are excluded from QBI.

A. How Section 199A Applies to Rental Income:

While the primary focus of Section 199A is on income from active trades or businesses, rental real estate activities can qualify if they meet specific criteria:

- Trade or Business Standard: To be eligible, the rental activity must rise to the level of a trade or business. Factors such as the taxpayer’s involvement in property management, frequency of rental activity, and the type of property rented are considered.

- Safe Harbor Rules: The IRS has established safe harbor rules for rental real estate to simplify the qualification process. This includes maintaining separate books and records for each rental enterprise, performing at least 250 hours of rental services annually, and more.

- Aggregation of Activities: Taxpayers with multiple qualified businesses can choose to aggregate them to calculate the QBI deduction. This allows for the offsetting of losses from one business against income from another.

B. Maximizing Tax Savings Through the Deduction:

To optimize the tax savings derived from Section 199A, taxpayers can employ various strategies:

- Aggregation Strategy: Consider aggregating multiple businesses to maximize the overall QBI deduction.

- Wages and Property Optimization: Since the deduction is subject to limitations based on W-2 wages and qualified property, managing these elements can impact the deduction amount.

- Tax Planning: Careful management of overall taxable income, through strategies such as timing income and deductions, can affect the availability of the QBI deduction.

- Professional Advice: Given the complexity of tax laws and the ever-evolving nature of regulations, seeking the guidance of tax professionals is crucial for personalized advice tailored to individual circumstances.

- Periodic Review: Tax laws are subject to changes, and periodic reviews of one’s tax strategy with a tax professional can ensure ongoing optimization of tax savings.

It’s essential to stay informed about any legislative changes and to consult with a tax professional to address specific circumstances and ensure compliance with the most current tax regulations.

Conclusion:

Navigating the realm of rental income and taxes requires a nuanced understanding of tax regulations and strategic planning. Small business owners can optimize their tax position by leveraging deductions, understanding depreciation rules, and staying abreast of changes in tax laws. To ensure compliance and maximize returns, consulting with a qualified tax professional is highly recommended.

Are you ready to unlock the full potential of your rental income and make informed tax decisions for your small business?

{kind=link}